Global geopolitics, tightening input supply chains and shifting cattle cycles are converging to reshape the outlook for Wagyu premiums, according to Episode 3 director Matt Dalgleish, when he spoke at WagyuEdge’26.

In a wide-ranging market briefing, Matt highlighted how current “unpredictable” global conditions, from Middle East tensions to trade dynamics are influencing both input costs and long-term opportunities for Australian Wagyu producers.

Input pressures intensifying amid global disruption

Matt began with a stark assessment of rising input risks, particularly in fuel and fertiliser markets.

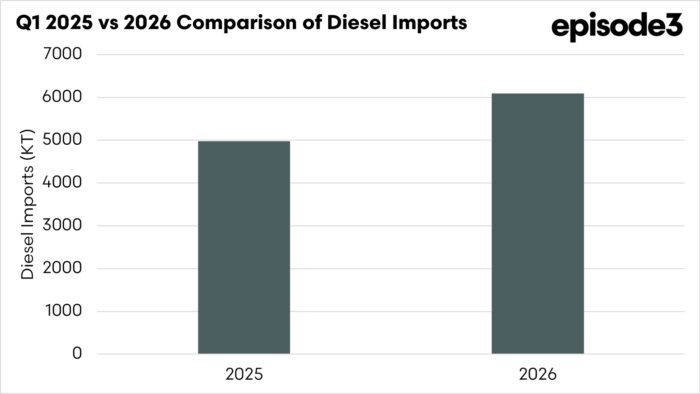

Volatility in crude oil prices following geopolitical conflict has already driven sharp increases in diesel costs, with Australia heavily reliant on imported fuel. Despite imports running 22% higher year-on-year in early 2026, spot market pressures have created short-term supply bottlenecks as buyers rushed to secure fuel.

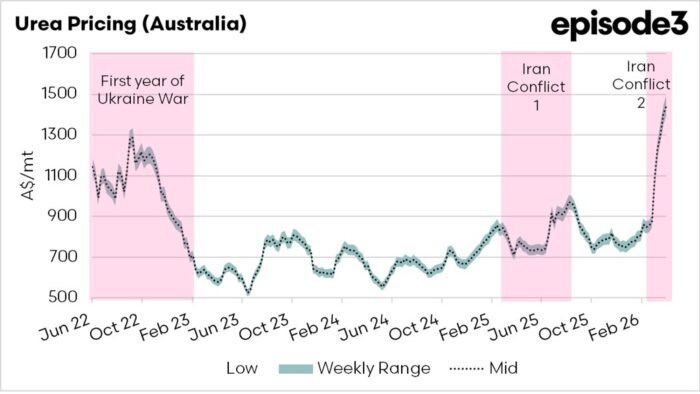

More concerning, however, is the fertiliser outlook.

Australia sources around 65% of its urea supply from the Strait of Hormuz, a region exposed to ongoing geopolitical instability. Dalgleish noted that current import flows sit at roughly 60% of last year’s levels, creating a potential 40% shortfall heading into the critical winter cropping period.

“This is not just a price issue, it’s also a physical supply issue,” he said, warning that shortages could persist for up to 18–20 months, based on historical comparisons with past energy shocks.

While grain prices have risen in response to higher energy costs, global wheat stocks remain relatively high, limiting the extent and duration of price spikes. This may offer some relief to feedlot operators, with Dalgleish suggesting grain markets are likely to ease later in the year.

Wagyu supply adjusts after 2025 pullback

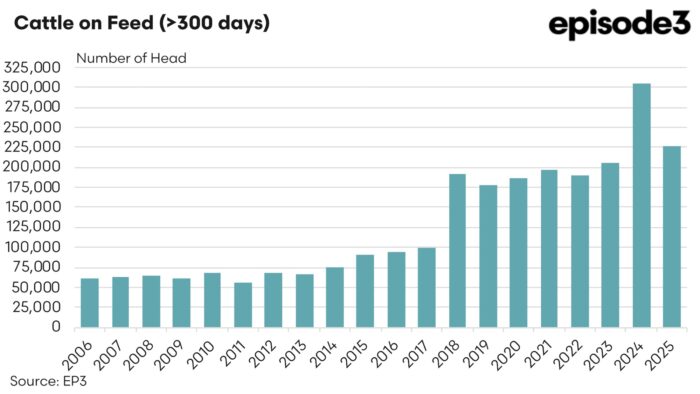

Turning to the Wagyu sector, Dalgleish highlighted a significant contraction in long-fed Wagyu supply through 2025, driven by weaker prices earlier in the cycle.

Estimates suggest the number of cattle on feed for more than 300 days, largely representing Wagyu, fell from a peak of just over 300,000 head in 2024 to around 227,000 head in 2025, a decline of roughly 25%. As a share of total feedlot cattle, Wagyu now sits at just over 6%, back in line with long-term averages.

This recalibration reflects the classic supply response to falling prices: production scaled back during the downturn.

However, more recent data indicates a recovery is underway.

Wagyu price premiums, particularly for higher-quality categories, have rebounded towards long-term averages after dipping below trend in mid-2025. Fullblood cattle proved more resilient during the downturn and are now leading the recovery, supported by continued demand for higher marbling beef.

Premiums stabilising, with quality driving gains

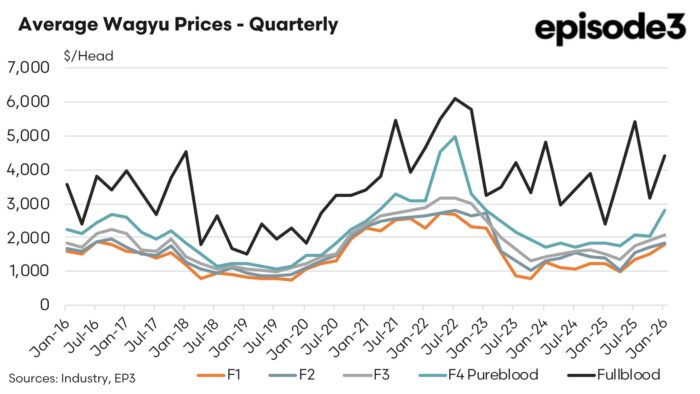

Matt emphasised that not all Wagyu segments are expected to benefit equally in the next phase.

While F1 prices are likely to stabilise, stronger upside is anticipated in higher-grade categories. “The gravitation toward higher marbling is continuing to support premiums at the top end,” he noted.

This aligns with broader market signals, including both domestic and international demand trends, where consumers are increasingly favouring premium product.

Strong export demand underpins outlook

Despite macroeconomic uncertainty, global demand for Australian beef remains robust.

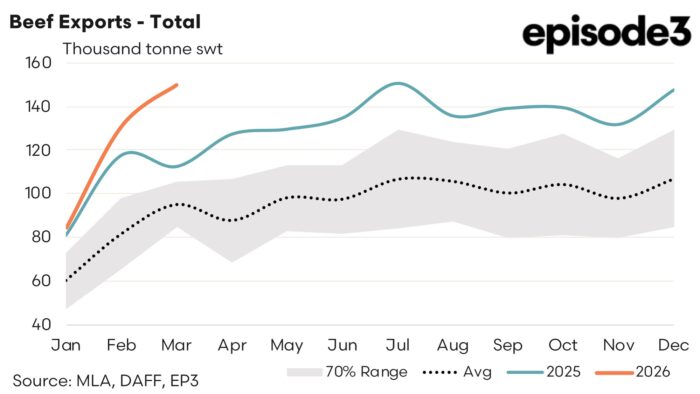

Australia recorded record beef exports in 2025, followed by an even stronger start to 2026. March volumes were among the highest monthly shipments on record, reflecting strong demand across key markets including the United States, China, Japan and South Korea.

China, in particular, has shown strong early-year demand, although Matt cautioned that the safeguard tariff mechanism could be triggered by mid-year, creating potential headwinds for exporters.

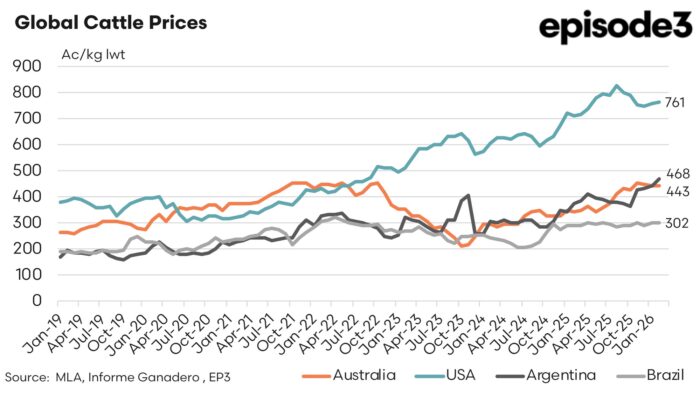

At the same time, tightening global cattle supply is expected to support prices. Many of the world’s major beef-producing countries are still in, or transitioning out of, herd liquidation phases, limiting supply availability.

Cattle cycle turning in producers’ favour

Domestically, Australia appears to be nearing the end of its recent liquidation phase, with key indicators such as the female slaughter ratio trending back towards rebuild.

Matt expects herd rebuilding to begin in earnest within the next six months, depending on seasonal conditions.

Globally, the United States is slightly ahead in the cycle, with cattle prices already elevated. US heavy steer prices are currently significantly higher than Australian equivalents, reinforcing a supportive international pricing environment.

Price outlook: gradual improvement ahead

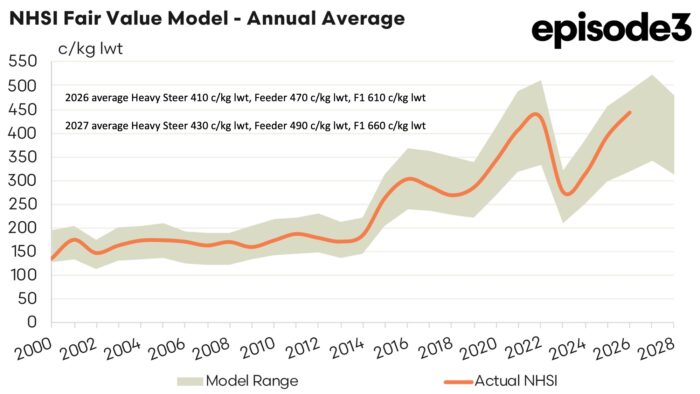

Looking forward, Matt forecasts steady gains in cattle and Wagyu prices over the next two years.

Key projections presented at WagyuEdge include:

- 2026 average prices:

- Heavy steer: ~410 c/kg liveweight

- Feeder cattle: ~470 c/kg

- F1 Wagyu: ~610 c/kg

- 2027 average prices:

- Heavy steer: ~430 c/kg

- Feeder cattle: ~490 c/kg

- F1 Wagyu: ~660 c/kg

Prices are expected to peak around 2027 before moderating slightly, though remaining well above historical lows.

Wagyu’s premium positioning offers long-term resilience

Despite near-term volatility, Matt remained confident in the longer-term outlook for Wagyu.

He noted that while rising input costs and geopolitical uncertainty present challenges, the underlying supply and demand fundamentals continue to favour producers.

“I think on balance, the underlying fundamentals are still incredibly robust in the favour of the producer,” he said.

A key factor underpinning this outlook is the continued global demand for high-quality beef.

Recent market behaviour has reinforced this trend, with higher marbling and fullblood Wagyu categories outperforming during periods of softer pricing. This highlights the resilience of premium product segments, which are less exposed to cyclical swings than lower-tier commodities.

Australia remains well positioned to capture this demand, supported by its reputation for consistent supply, product integrity and access to key export markets.

However, Matt cautioned that the operating environment is becoming more complex. Trade settings, input costs and broader economic conditions will all play a role in shaping outcomes in the years ahead.

“There are some dark clouds, particularly what’s happening currently in the Middle East and the flow‑through to those energy prices,” he said, noting the potential for inflation and slower economic growth to influence global demand.

In this environment, maintaining Wagyu’s premium positioning will require continued focus on quality, efficiency and market access.

Balancing opportunity and risk

While rising Wagyu and cattle prices offer a positive outlook, Matt cautioned that input cost pressures could offset some gains.

“There are some dark clouds,” he said, pointing to inflationary risks, higher interest rates and potential economic slowdowns if energy costs remain elevated.

However, the overall balance of supply and demand remains supportive.

“I think on balance, the underlying fundamentals are still incredibly robust in favour of the producer,” Matt concluded.

For Australian Wagyu producers, the message is clear, while volatility is here to stay, tightening supply, strong global demand and a shift towards higher quality are setting the stage for a renewed period of opportunity, provided input risks can be managed.